Dividends and capital gains are two different forms of income that we may receive from investments. Dividends come from stocks, while capital gains come from the sale of assets such as stocks, real estate, gold. But dividends vs. capital gains which is better?

It is a question that has been asked for decades, and the answer is not always clear. Which one should you invest in? What are the economic growth potentials of each type of investment? And what about taxes? In this post, we will explore all of these questions to help you make an informed decision on which type of investment best suits your needs.

Difference between dividends and capital gains (dividends vs. capital gains)

Dividends and capital gains are two different types of returns on investments.

Stock dividend income provides an investor with periodic payments. A corporation shares its profit with shareholders in the form of dividends.

Dividends can be paid in cash or shares and are typically paid on an annual basis. It’s often considered one of the safest and most reliable ways to invest your money, especially if you want predictable returns on your investment.

On the other hand, a capital gain can result from selling any type of property — real estate, stocks, bonds, mutual funds, etc. The amount realized by the sale must exceed your basis plus expenses incurred during ownership.

For example, if you purchased shares of XYZ Company Inc. for $10 per share and then later sold them for $20 each, you would have a capital gain of $10. It’s taxed either short-term or long-term based on how long the stocks were held before they were sold.

Is dividend income better than capital gains?

If you look at the returns of stocks over the last century, it might appear that investment income from dividends is better than capital gains. Stocks have historically given a return of about 10% per year. If you were to calculate the total return by taking into account both dividends and capital gains, then your results would show an average yearly return of around 11%.

The difference between the two is mostly due to the fact that about 5% of stocks’ returns each year come from dividends while 6% comes from capital gains. Since dividends are taxed at a lower rate than capital gains, dividend income seems like it would be better for your individual tax bill.

However, there’s more to dividend taxation than meets the eye. There are actually three different types of capital gains tax rates: zero percent, 15%, and 20%.

Let’s say that you’re an average American taxpayer who follows the rules. In a year where your income falls within the 15% marginal tax bracket, then any dividends or capital gains that you receive will be taxed at a rate of 15%. In other words, you will actually be taxed at a lower rate than what is advertised.

Dividends may not always give you the “better” tax treatment. Even if dividends are taxed at a zero percent capital gains rate, which they normally are for taxpayers in the 15% tax brackets, there’s still no guarantee that dividend income is better than capital gains.

For people in the zero percent tax bracket, they will actually pay more taxes on dividends than on capital gains. That happens when dividend income pushes you into a higher tax bracket.

For example, say that Mr. A has a taxable income of $9,000 per year ($750 per month). He invests in a stock fund that gives him a 10% yield on his investment. In that case, Mr. A would receive $75 of dividend income per month and have no capital gains or losses to report. On paper, it looks like he’s getting the better tax deal by having his dividends taxed at a zero percent rate compared to a 15% tax rate on capital gains.

But what if his taxable income rose to the point where he was in the 10% tax bracket? In this case, Mr. A would see $99 per month go towards taxes as opposed to only $75 monthly, which is what he’d pay if he had invested in an investment that gave him 10% returns through dividends instead of capital gains.

People who receive dividend income are generally older individuals who live off their investments, so it’s rare for them to be pushed into a higher tax bracket purely because of the dividends that they receive. However, that age group is not free from taxation on capital gains either.

If you’ve held onto your stocks long enough to qualify for the zero capital gains tax rate, then every dollar that you make from capital gains is a dollar that you don’t have to pay taxes on. In this case, it’s true that dividend income may not always be better than capital gains. However, there are other factors to consider as well.

Dividend payments fluctuate from year to year. If you’re living on a fixed income, then it’s best to choose investments that come with dividends that are more stable and not as likely to fluctuate.

You also need to take into account the amount of time and effort that you’ll need in order for your investments to pay off. There’s no point investing in stocks if you don’t have the time to watch over them and manage your portfolio. If this is a problem, then you may want to avoid stocks altogether and choose something less volatile yet still produces competitive returns.

On the other hand, dividend distributions also offer more flexibility when it comes to finding new investments. In addition, dividend payments are taxed at more favorable rates as an ordinary income rate than capital gains.

Another factor to consider is how your investments will be taxed in the future. Right now, income from dividends and capital gains are taxed at different rates. But there’s no saying what the government may do tomorrow.

Therefore, you should diversify your portfolio so that it contains both dividends and capital gains instead of putting everything into just one basket.

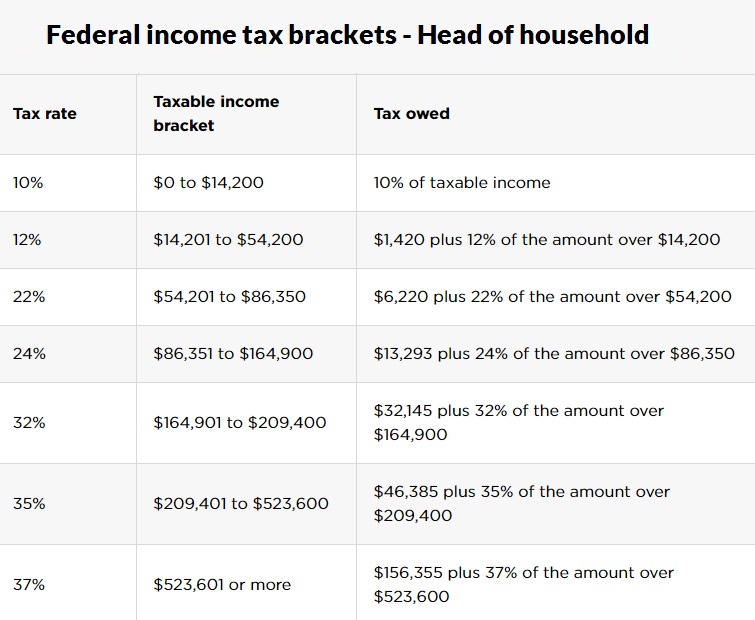

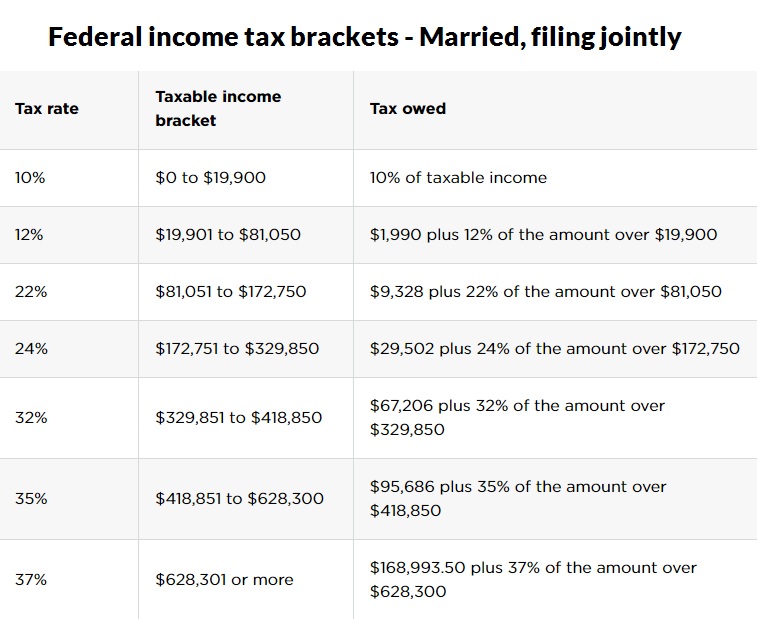

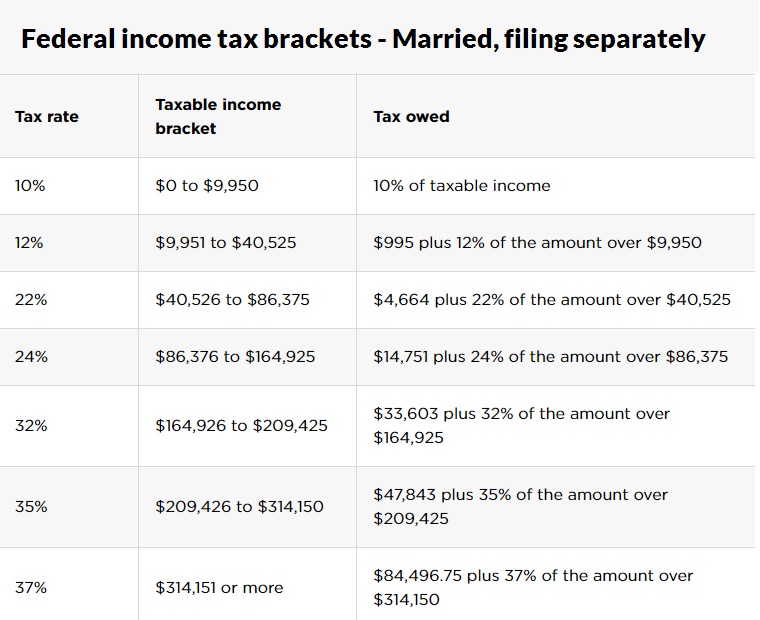

Capital gains and dividends tax rates

Dividends are taxed at a lower rate than capital gains.

Dividend income is taxed the same as interest or other types of ordinary income, depending upon the investor’s tax rate. The effective tax on dividends depends on what income strata or level of income you are in.

Capital gains are taxed at the same rate as interest income or dividends, depending on what you qualify for.

However, Capital gain tax is calculated based on either short-term gains or long-term gains.

Capital gains within one year period are considered a short-term capital gain. Short-term capital gains are taxed as the ordinary income tax rate.

Long-term capital gains, which apply to assets owned more than a year and a day. This form of capital gain has three tax slabs: 0%, 15%, and finally, the maximum long-term capital gains tax rate is 20%.

The IRS considers any money received from selling shares of stock as “capital gain.” This means that investors can deduct up to 30% of their total gross income against their federal income taxes. Investors must file Form 8949 to claim these deductions.

The maximum deduction allowed depends on several things, including whether the investor itemizes their expenses on Schedule A of their return, whether the individual owns real estate, and whether the individual lives in a high-tax state such as New York, California, Massachusetts, etc.

The IRS allows taxpayers to deduct up to 30% of adjusted gross income against ordinary income. This means that someone making $100,000 can claim a total of $30,000 in deductions against their AGI.

In general, investors must include all of their qualified dividends and capital gain distributions in calculating their AGI.

Qualified dividends are those paid by corporations whose stock has been owned continuously for three years or longer. Dividends received from publicly traded companies are considered qualified dividends.

Qualifying dividends are subject to U.S. federal government income tax, but state and local taxes are deductible. So, for example, if a taxpayer receives $1,500 in qualifying dividends and pays 25% sales tax, she could subtract $375.

What To Do Next If You Have Both Types of Income Dividends and Capital gains?

If you have both types of income, dividends, and capital gains, your tax situation is a little more complicated. Tax rates for your dividends are lower than those for capital gains, so you’ll want to make sure that the majority of your investment income falls into this category.

You will be able to avoid double taxation of dividends if you own mutual funds and your mutual fund company takes the 20% deduction on qualified dividends before applying the 39.6 percent top rate for capital gains, which is often the case with funds that invest in blue-chip stocks.

As an example, let’s assume you have $80,000 in long-term capital gains. If half of your capital gains come from mutual fund dividends and a half from selling stock, you would owe taxes on only half the amount—$40,000—at a 15 percent rate for qualified dividends. So in that scenario, you could owe 20 percent of $40,000 or $8,000.

What are the risks associated with stock capital gain?

The main risk associated with a stock capital gain is that there is no guarantee that the stock value will always rise. If you invest your money in stocks, you are exposed to the risk of capital losses due to unfavorable economic, political, or market conditions. These risks are called trading risks because they arise when you trade financial instruments.

On the other hand, the risk profile is not that high in dividend investing. Because most dividend-paying stocks tend to be established companies with a proven business profit, so it’s very unlikely that they will go bust – unless you’re investing in a company with poor financial condition.

Generally, the company pays regular dividends; It’s almost certain that the stock price will rise or remain stable. Moreover, the rate of dividends remains stable year after year. But The rates on capital gains are not stable.

However, do not confuse unrealized capital gain with a capital loss. Capital gains are realized only when one sells a financial instrument at a price higher than the price he bought it. Conversely, a capital loss occurs when one sells a financial instrument at a price lower than the price he bought it.

However, In reality, you can lose both capital and dividends from an investment if your holding period is too short. If your goal is to hold stocks for the long term, then go for a well-established company with a good stock dividend yield.

When capital gains are preferable over dividends

Capital Gains Can Be Used For Building Wealth Over Time

If you don’t mind waiting until after retirement to start enjoying the fruits of your labor, then capital gains might be more appropriate than dividends because you won’t be able to use them to cover your lifestyle. This is especially true if you expect to spend most of your time working during retirement.

Capital Gains Are Not Taxed Twice

When you buy an asset for $15,000 and sell it later for $30,000, the tax burden is lighter than if your purchase was made with dividends because dividend income will be taxed at whatever marginal rate you are at that time. This can mean a difference of over 50% in the amount of taxes you pay.

Capital Gains Are Not Tied To Your Income Level

Dividends and interest income will be given a lower tax rate if they fall under the maximum earning limits. This means that your effective tax rate can vary widely depending on how much money you make in dividends. Capital gains are not linked to this system of the marginal tax rate, so short-term capital gains are taxed at the same rate regardless of whether you are an employee or self-employed. This makes capital gains significantly more desirable than dividends for anyone who needs to cover their living costs but has already hit the maximum income limit set by the government.

Capital Gains Are Not Subject To The Alternative Minimum Tax (AMT)

This is an important point. People may be surprised to learn that dividends are subject to the AMT (Alternative Minimum Tax), which means that they could end up being taxed at a higher rate than capital gains in certain circumstances. Basically, if you find yourself in this situation, you should pay the AMT instead of using dividends.

Conclusion

I have to admit this is a difficult question. It depends on what your investment objective is for the market and how long you plan on being invested. I would encourage you to speak with an experienced financial advisor (financial planner) before making any decisions about which type of investment might be best suited for your needs.

As always, do not invest unless you can afford to lose all the money that you will put into it because the stock market has ups and downs. In addition, dividends have default risk, and that is inflation risk. It’s better to calculate the inflation rate before making any investment decisions.

You may also want to consider seeking advice for better tax efficiency from a qualified tax professional if there are applicable favorable tax rate implications associated with one type of dividend versus another.