Many parents are unaware of the option to endorse a check on behalf of their child. Recently, I encountered a scenario where my fiancée needed to endorse a check for her niece. At first glance, it seemed like a straightforward task. However, the realization that her niece wasn’t of legal age added a layer of complexity to the situation.

Upon delving into the matter further, I discovered a solution: it is indeed possible to legally endorse a check for an individual under the age of 18, provided there is parental consent. This revelation shed light on an often overlooked aspect of financial management for minors.

Endorsement, in essence, involves the act of signing over one’s rights to what they own or owe. In the context of endorsing a check for a minor, it serves as a mechanism to transfer ownership of the funds to the child. Understanding this process not only ensures compliance with legal requirements but also empowers parents and guardians to navigate financial matters more effectively on behalf of their children

Can I deposit my child’s check into my personal account

Parents are free to deposit their children’s checks into their own personal bank accounts as they are the minors’ legal guardians. However, the bank may require the parent to provide identification and proof of guardianship before accepting a child’s check for deposit.

Some banks have policies in place that restrict account holders from endorsing others’ checks, known as a third party check.

But most of the banks will accept your check if you follow their endorsement and inclusion requirements for your child’s name or signature, as well as yours.

Endorsing a check for a minor: Two Easy Steps

Endorsing a check for a minor is a common practice in the banking industry. For this reason, some customers may wonder why a bank will not simply accept a check for a minor.

However, it completely depends on your bank or credit union because different credit unions and banks have their own security policy.

Although some banks might have more relaxed policies than others, most strongly adhere to federal law in this matter.

Endorsing a check made out to a minor is a relatively simple process and can be completed in two steps:

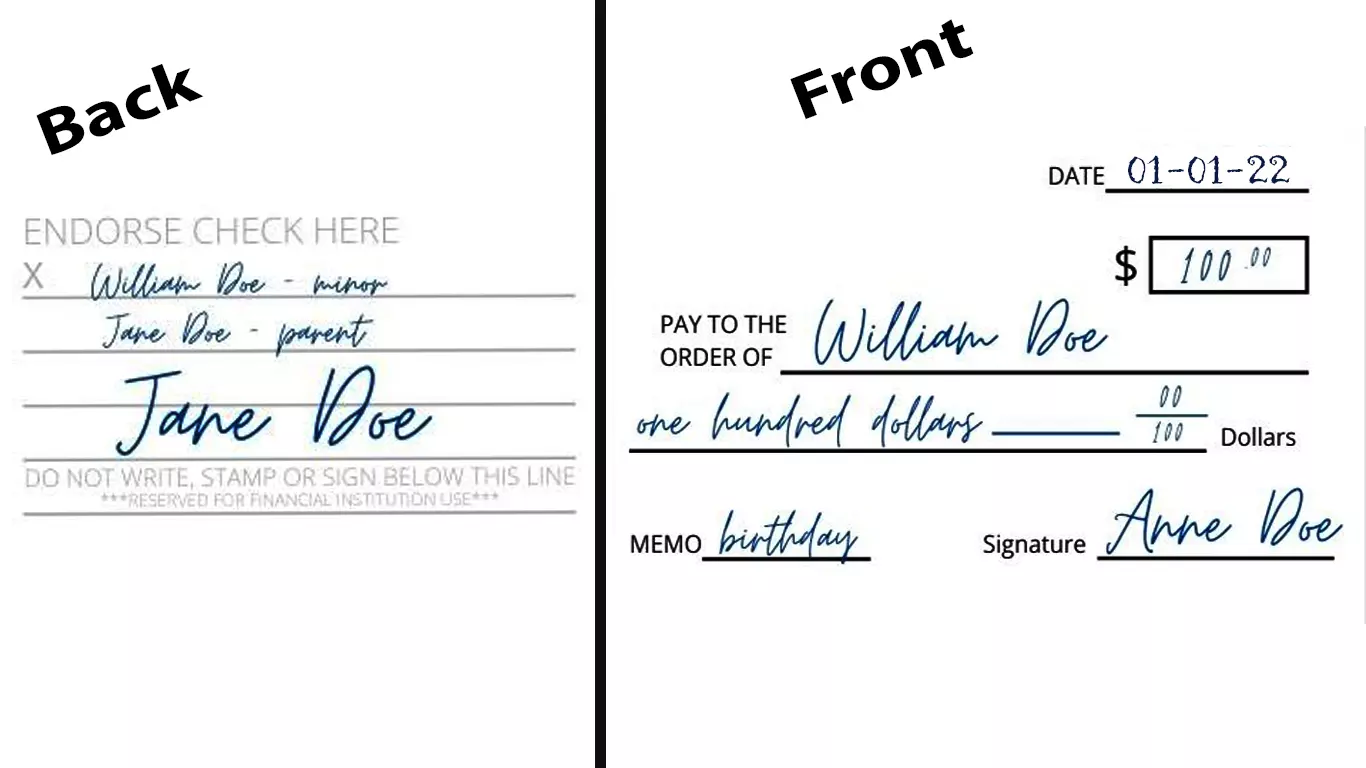

- In the endorsement area on the back, You will have to write the child’s name with a hyphen and the word “minor” to indicate they are a child.

- Then, write your name with a hyphen that indicates your relationship with the child, like mother, father, parent, or guardian. Finally, sign your name to finish endorsing the check.

If you are drawing a check to a minor, it is important to make it out to the parents. The amount written in the memo line should be “For The Benefit Of” the Minor.

It’s a good practice to write the minor parent’s name on the Pay to the Order line of the check. This way, it becomes clear who is taking care of the check and makes it easy for the parents to handle the money.

Can a minor have a Bank Account

Yes, a minor can have a bank account if they have parental approval and identification. In this situation, it will be considered a custodial account.

All custodial account money is the property of the minor, who may take complete ownership at age 18, and a parent or legal guardian is in charge of the account on behalf of the kid.

However, because banks cannot do contracts or legal agreements with people under the age of 18, a minor can’t open their own bank account or cash their checks.

How to Open a Minor’s Account

You will need to provide proper identification for both you and your child. Bring your government-issued photo ID and your child’s social security card. If the minor is under 12 years, then you can bring your child’s birth certificate.

Once you are at the bank, make sure that you take care of all documentation needed to open an account for your child. You may be asked to fill out the account application form, which you can also fill up later on at home.

On the form, provide your child’s personal information such as date of birth, current address, and telephone number.

You will have to choose an account type such as a savings account or current account that best suits your needs or your child’s needs.

You should take time to compare each service before making a decision on the type of account to open.

If your bank offers online accounts, you can have your child sign up for one as well; this way, you can perform transactions like transferring funds and checking account balances on their own. You can also use a mobile deposit service using banks’ mobile apps.

The method of depositing a check is the same, regardless of which service you choose to establish for your child.

The minor can sign the back of the check and write his or her account number. This is an excellent technique for kids to learn how to save money at an early age.

What are the Benefits of a child having their own bank account

A child with a bank account is more likely to learn about money and saving at an early age. Bank accounts for kids also help teach financial responsibility.

The logic is that if they start saving early, then they’ll be able to save more and end up with a healthier financial situation later on. That argument has finally convinced many parents who are now opening accounts for their kids at an increasing rate.

Plus, when parents set up a bank account for their children, it can help them establish credit early on in life.

According to research, having a children’s bank account increases their chances of accumulating assets and becoming good investors in the future.

Bottom Line:

The process for endorsing a check for a minor is not complicated. It’s important to understand what you have to write on the back of the check. For example, you can follow the above image for endorsing a minors’ check. Here “William Doe” is the minor, and “Anne Doe” is the check writer. And finally “Jane Doe” is a parent of the Minor.

If you’re the parent of a minor, it is important to keep in mind that most banks will not allow minors to open an account on their own. You may be able to deposit your child’s check into your personal bank account if they are added as an authorized user or joint owner with rights of withdrawal and signing authority over the checking account.

However, a better option would be for parents to set up custodial accounts for their children. You can establish a custodial account at a bank or credit union or any other banking institution that offers this type of service.

Make sure you contact the customer service of your financial institution to know the rules before you set up a form of account.